Many Australians spend years carefully planning for retirement.

They think about when they will stop work. They estimate their superannuation. They check their Age Pension entitlement. They consider whether to downsize, renovate, travel, help family, or simply enjoy a more comfortable lifestyle.

But there is one planning question that is often underestimated:

How long might your retirement actually last?

It is an important question, because many retirees are not just planning for the next few years. They may be planning for 15, 20, 25 or even 30 years of retirement.

That has a major impact on how much cash you may need, how you access it, and how a reverse mortgage should be structured.

At Seniors First, we often speak with older homeowners who are “asset rich but cash poor”. They may own a valuable home, but still feel squeezed by day-to-day living costs, rates, insurance, home maintenance, medical expenses, car replacement, or the simple desire to enjoy life a little more.

For some, a reverse mortgage can help bridge that gap.

But the key is not simply asking, “How much can I borrow?”

A better question is:

“How much might I need over time, and what is the smartest way to access it?”

That is where longevity planning becomes so valuable. Thankfully, the Government publishes longevity tables so anyone can find out – statistically – how much living they have left.

Why longevity matters in retirement funding

Most people understand that Australians are living longer. But many do not fully apply that reality to their own budget.

It is common for retirees to think in short timeframes:

- “I need $30,000 for home repairs.”

- “I need to clear the credit card.”

- “I want to replace the car.”

- “I just need a bit extra each month.”

- “I’ll probably downsize eventually.”

Those are all valid needs. But they are only part of the picture.

KEY FACT: a statistic that might surprise you is that a 60 year old woman in good health today has a 50 per cent chance of living to age 90. That’s 30 more years of living!

So your retirement funding may need to last into your 80s or 90s. If you are 70, you may still need to plan for another 15 to 20 years. If you are part of a couple, planning becomes even more important because the loan may need to support the surviving partner for many years after the first partner passes away or moves into care.

A reverse mortgage is a long-term financial product. That means the loan structure matters.

Borrowing too much upfront can increase interest costs unnecessarily, because interest compounds over time. Borrowing too little, or failing to plan for later needs, can leave you short of funds when you may need them most.

The aim is to find a sensible balance.

A simple two-step planning exercise

Before choosing a reverse mortgage structure, many borrowers benefit from doing two basic planning exercises.

Step 1: Prepare an annual cashflow budget

To prepare budget, start with your regular income. This may include the Age Pension, superannuation pension payments, account-based pension income, investment income, rental income, or other sources.

Then list your regular expenses, including:

- groceries

- utilities

- council rates

- strata levies, if applicable

- home insurance

- health insurance

- medical costs

- transport

- car registration and servicing

- home maintenance

- family support

- hobbies, outings and social activities

- holidays or special events

This helps identify whether there is a regular shortfall.

For example, if your retirement income is $34,000 per year but your comfortable living expenses are closer to $42,000 per year, you may have an annual shortfall of around $8,000.

That does not automatically mean you should borrow $8,000 every year forever. But it does help clarify the size of the problem.

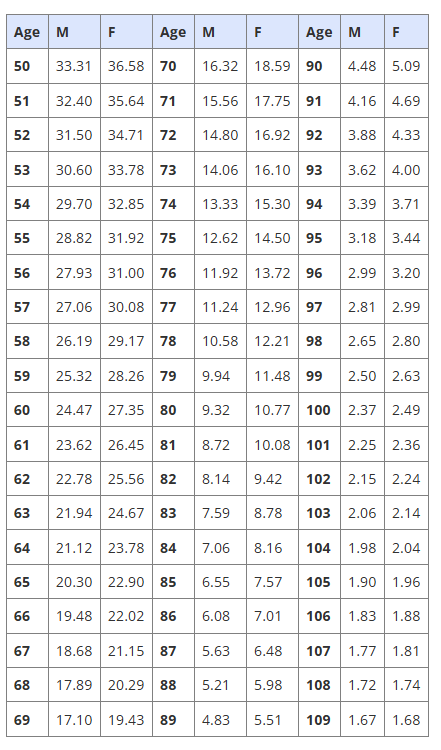

Step 2: Consider expected longevity

The Australian Government publishes life expectancy tables that show the average number of additional years a person of a given age may be expected to live.

These tables are not a personal prediction. Nobody knows exactly how long they will live. Your health, family history, lifestyle, and personal circumstances all matter.

But the tables are useful because they give retirees a practical planning guide.

For example, a person aged 65 may have a life expectancy of around 20 to 23 more years, depending on whether they are male or female. A person aged 70 may still have around 16 to 19 more years. A person aged 75 may still have around 13 to 15 more years.

That can be a surprise.

Many people in their late 60s think of themselves as “well into retirement”. But in funding terms, they may still need a plan that lasts two decades.

Turning longevity into a funding estimate

Once you have your annual cashflow shortfall and your approximate life expectancy, you can start to estimate your medium and long-term funding need.

For example:

Annual shortfall: $8,000

Estimated planning horizon: 20 years

Potential lifetime shortfall: $160,000

This does not mean you should take $160,000 as a lump sum on day one.

In fact, in most cases, that may be the wrong structure.

The purpose of the exercise is to help you and your broker understand the scale of your future need. From there, the loan can often be structured more carefully.

A reverse mortgage may allow funds to be accessed in different ways, such as:

- an upfront lump sum

- regular instalments

- a cash reserve or redraw-style facility

- a combination of these

The right mix can make a significant difference to long-term interest costs.

Why loan structure is so important

With a reverse mortgage, you generally do not need to make regular repayments while you live in the home. Instead, interest is added to the loan and repaid later, usually when the property is sold, you move permanently into aged care, or the estate is finalised.

This can be very helpful for cashflow.

But it also means the timing of your drawdowns matters. In terms of how Reverse Mortgages work, there are three ways you can take the funds: lump sum, regular instalment and cash reserve.

The more you borrow upfront, and the longer the money is outstanding, the more interest may compound over time. That is why a carefully structured loan may be better than taking one large lump sum unnecessarily.

At Seniors First, we have long encouraged borrowers to consider drawing only what they need upfront, then setting aside future access through instalments or a cash reserve where suitable. This approach is designed to help borrowers access the money they need while avoiding unnecessary interest on funds they do not yet require.

In simple terms:

Borrowing everything upfront may feel convenient, but it can be expensive.

Borrowing gradually, where appropriate, may help preserve more home equity over time.

Example 1: The couple with home repairs and future care needs

John and Helen are both 72. They own their home but have limited savings.

Their immediate need is $45,000 for essential home repairs, including bathroom modifications, safer flooring, and electrical work. These improvements will help them remain at home more comfortably.

They also have a small annual cashflow shortfall of around $5,000.

At first, they ask whether they should simply borrow $150,000 to “be safe”.

But after reviewing their budget and likely future needs, their broker suggests a more staged approach.

The structure also recognises that their needs may change. They may stay at home for many years. One partner may need care before the other. They may eventually choose to downsize. Or they may simply need extra funds from time to time.

A flexible reverse mortgage structure can help keep options open.

Example 2: The future downsizer

Robert is 76 and lives alone in a home that has become too large for him. He knows he may downsize one day, but he is not ready now.

He is worried about selling in a soft property market and does not want to rush into a major lifestyle decision.

His immediate needs are:

- $25,000 for home maintenance

- $20,000 to replace his car

- around $6,000 per year to improve cashflow

He expects he may sell the home in three to five years, but he is not certain.

For Robert, the reverse mortgage may act as a “downsizing alternative” or a bridge.

A possible loan structure might include:

- a lump sum for the car and repairs

- a cash reserve for unexpected costs

- limited regular instalments to support cashflow until he decides whether to sell

This gives Robert time.

Instead of being forced to sell quickly, he can stay in control and make a calmer decision when the time is right.

The danger of under-provisioning

One of the risks we see is retirees under-provisioning for the true length of retirement.

This can happen for several reasons.

Some people are naturally cautious and do not like debt. Others worry about leaving less inheritance. Some assume they will downsize later, but the years pass and they remain in the same home. Others underestimate inflation, healthcare costs, strata levies, home maintenance, or the cost of getting help around the house.

The result can be a loan that solves today’s problem but does not properly consider tomorrow’s.

For example, a borrower may release $40,000 to clear debts and pay bills, but make no provision for the next 10 years of income shortfalls. A few years later, they may need to come back for more funds.

IMPORTANT: it’s usually possible to get a ‘top up’ in future, but it’s never guaranteed. Top ups are a post-settlement loan process that’s technically a new credit application. Your ability to get additional funding in future from your lender will depend on many variables at that time: your property’s value, your age, lender credit criteria and rules, available equity and product limits.

A better approach is to consider future needs at the beginning, even if those funds are not drawn straight away.

This is where a specialist reverse mortgage broker can add real value.

Why a specialist broker matters

Reverse mortgages are not ordinary home loans.

They involve older borrowers, long-term compounding interest, estate considerations, Centrelink and Age Pension issues, family discussions, aged-care possibilities, and the emotional importance of the family home.

A general loan comparison is not enough.

At Seniors First, our role is to help older Australians understand their options clearly, compare lenders, and structure loans in a way that is suited to their needs.

That may include:

- comparing different reverse mortgage lenders

- identifying suitable loan features

- considering lump sum, instalment and cash reserve options

- explaining the effect of compounding interest

- helping borrowers avoid drawing more than they need upfront

- looking at future top-up needs

- helping preserve more home equity where possible

- coordinating the application process from start to finish

Our HomeEquiSaver™ approach is built around a simple principle:

Access the equity you need, but structure the loan carefully so you are not paying interest on money before you need it.

This is especially important when longevity is part of the conversation.

If your retirement may last another 10, 15 or 20 years, then the structure of your reverse mortgage can matter just as much as the interest rate (even more so).

A practical planning framework

If you are considering a reverse mortgage, here is a simple framework to discuss with your broker.

1. What do you need immediately?

This may include debt repayment, home repairs, car replacement, medical bills, or urgent cashflow relief.

These needs may be suitable for an upfront lump sum.

2. What is your annual shortfall?

Prepare a simple yearly budget. If your income does not meet your expenses, estimate the gap.

This may point toward a regular instalment plan.

3. How long might the shortfall last?

Use life expectancy tables as a guide, but also consider your health, family situation and plans for the home.

This helps estimate the medium and long-term funding requirement.

4. What future costs could arise?

Think about home maintenance, health needs, in-home care, strata levies, mobility changes, and possible aged-care transitions.

This may support having a cash reserve.

5. What equity do you want to preserve?

Many borrowers want to preserve equity for future aged care, downsizing, a surviving spouse, or inheritance.

This should be part of the loan structure discussion.

6. What happens if plans change?

A good structure should allow for uncertainty. Retirement is rarely perfectly predictable.

You may live longer than expected. You may choose not to downsize. You may need help at home. You may want to assist family. Or you may decide later that you need less than originally planned.

Flexibility matters.

The goal is not to borrow more. It is to borrow smarter.

Longevity planning is not about encouraging retirees to borrow the maximum amount available.

Quite the opposite.

It is about helping borrowers make more informed decisions.

If your expected retirement is longer than you realised, you may need to plan more carefully. But that does not mean taking a large lump sum unnecessarily.

In many cases, the smarter approach is to:

- solve immediate needs with a modest lump sum

- support ongoing income needs with instalments

- keep a cash reserve for future uncertainty

- avoid paying interest on funds before they are required

- review the structure as life changes

That is the difference between simply taking a reverse mortgage and properly structuring one.

Final thoughts

Living longer is a wonderful thing. But it also means retirement funding needs to stretch further than many people expect.

For older homeowners, the family home may be more than a place to live. It may also be an important financial resource that can support comfort, independence and choice in later life.

A reverse mortgage can help some retirees access that wealth without selling the home. But the most important question is not just how much equity is available.

The better question is:

How can that equity be accessed safely, carefully and efficiently over time?

By combining a simple annual cashflow budget with life expectancy planning, borrowers can get a clearer picture of their future funding needs.

From there, a specialist reverse mortgage broker can help structure the loan using the right mix of lump sum, instalments and cash reserve.

At Seniors First, we believe this careful approach can help older Australians enjoy greater confidence today, while still protecting more choices for tomorrow. It may help to read some of our real case Reverse Mortgage customer case studies .

If you would like to understand how much equity may be available in your home, and how a reverse mortgage could be structured for your needs, speak with a Seniors First reverse mortgage specialist.

We will explain your options clearly, compare lenders, and help you decide whether home equity release is right for you.

Disclaimer: The information provided on this blog is for educational and informational purposes only. It does not constitute financial, investment, or legal advice. Please consult with a licensed financial professional before making any investment decisions.