The rising cost of living in Australia impacts everyone, but it’s especially tough for older Australians living on fixed incomes. Let’s face it, it’s not easy seeing your budget stretched thinner and thinner each month.

Housing costs are through the roof, with rent and property prices climbing steadily. This means less money for other essentials, which can be particularly challenging for seniors.

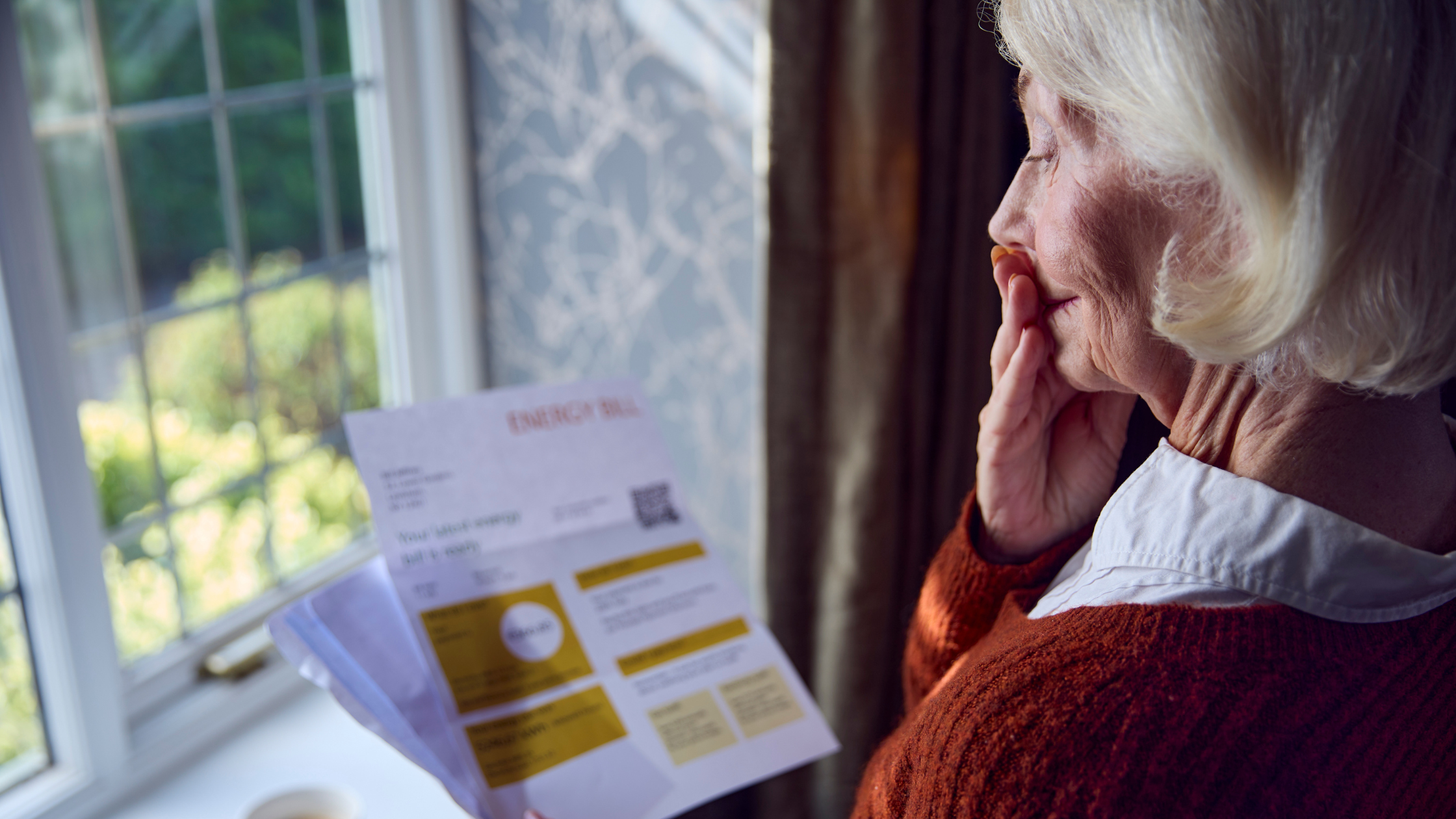

Then, there are the utilities—electricity and gas prices have jumped, with the Australian Energy Regulator reporting significant increases in some areas last year. No one wants to be stressed over their monthly bills, right?

Healthcare costs are another big worry. Even though Medicare helps, the out-of-pocket expenses for medications, specialist visits, and procedures can add up quickly. And let’s not forget grocery prices; they’ve been creeping up too, thanks to supply chain issues and environmental factors, making it harder to maintain a healthy diet.

All these rising costs can lead to financial stress and tough choices about where to cut back. But here’s the thing: constantly cutting back isn’t a sustainable solution. It can lower your quality of life, affect your health, and lead to financial instability in the long run.

In this blog, we’ll dive into why relying solely on cost-cutting isn’t the answer and explore alternative strategies to help you manage rising living expenses more effectively.

[ RELATED POST: Breaking Point: Cost of Living Hits Australia’s Seniors ]

Limited Scope of Cost-Cutting

When it comes to managing your finances, cutting costs might seem like a straightforward solution. However, cost-cutting has its limits and can’t address all your financial needs.

Some expenses are unavoidable or difficult to reduce significantly, including:

- Eating a balanced diet is vital for good health. Opting for cheaper, less nutritious options to save money can negatively impact your overall health.

- Health, home, and car insurance are necessary for your protection and peace of mind. Skimping on these could leave you vulnerable in emergencies.

- Home and vehicle maintenance costs are often unpredictable but essential. Ignoring small repairs can lead to bigger, more expensive problems down the line.

- Services like dental check-ups, vision care, and hearing aids are crucial for maintaining your quality of life. Reducing spending in these areas can lead to health issues that are costly to address later.

- Whether it’s public transport fares, fuel for your car, or occasional travel to visit family and friends, travel expenses are part of staying connected and maintaining your lifestyle. Cutting back too much can limit your mobility and independence.

- Phone and internet bills are essential for staying in touch with loved ones and accessing important information and services.

- Maintaining a comfortable and safe home is essential. Skimping on home maintenance or repairs can lead to a less safe and pleasant living space.

While trimming unnecessary expenses is always a good practice, relying solely on cost-cutting has its limitations. Some costs are unavoidable, and reducing spending in certain areas can negatively impact your quality of life and health.

Alternatives to Cost-Cutting for Managing Rising Costs of Living

If you’re finding that cutting costs isn’t enough to manage rising living expenses, there are several alternatives that can help you handle your finances more sustainably. Let’s explore some effective strategies.

Seeking Government Assistance and Benefits

There are various government programs designed to help older Australians. Make sure you’re receiving all the benefits you’re entitled to, such as:

- Age Pension: Provides a regular income for eligible older Australians. Learn more at the Department of Social Services.

- Pensioner Concession Card: Offers discounts on health care, medicine, and other costs. Details can be found on myGov.

- Commonwealth Seniors Health Card: Provides similar benefits for those not eligible for the Pensioner Concession Card. More information is available at Services Australia.

- Rent Assistance: Helps with the cost of renting a home. Find out more on Services Australia.

Budgeting and Financial Planning with Professional Help

Working with a financial planner can help you create a realistic budget and financial plan. A professional can offer tailored advice on managing your money, investing wisely, and preparing for future expenses. This guidance can make a big difference in your financial stability and peace of mind.

Exploring Part-Time Work or Passive Income Opportunities

If you’re able, taking on part-time work can provide a valuable income boost. Here are some part-time work opportunities:

- Retail or Hospitality Jobs: Many stores and cafes look for part-time staff, especially during busy seasons.

- Consulting or Freelance Work: Use your professional skills in a freelance capacity.

- Tutoring: Share your knowledge in subjects you are proficient in.

- Customer Service Roles: Many companies offer part-time customer service positions, often with flexible hours.

Alternatively, look into passive income opportunities, which can provide income with less active involvement. Here are some options:

- Renting Out a Spare Room: Platforms like Airbnb make it easy to rent out extra space in your home.

- Investing in Dividend-Paying Stocks: Earn regular income through dividends from shares in profitable companies.

- Creating an Online Course: Share your expertise by creating a course on platforms like Udemy.

- Writing an eBook: Publish your own book and earn royalties from sales.

These additional income streams can help cover expenses without the need for drastic cost-cutting. By combining part-time work and passive income opportunities, you can create a more secure and flexible financial situation.

[RELATED POST: Australian government encourages more pensioners to go back into work ]

Reverse Mortgage: Unlocking Home Equity

A Reverse Mortgage can be a powerful tool for older Australians to access additional funds without needing to cut costs drastically.

Unlike a traditional mortgage, you don’t need to make regular repayments. Instead, the loan, along with interest and fees, is repaid when you sell your home, move into aged care, or pass away.

How does a Reverse Mortgage work?

- Eligibility: Generally, you must be aged 60 or older to qualify for a reverse mortgage. The amount you can borrow depends on your age and the value of your home.

- Receiving Funds: You can choose to receive the funds as a lump sum, a regular income stream, a line of credit, or a combination of these options.

- No Repayments: You don’t have to make any repayments while you live in your home. The loan is repaid when the property is sold, usually from the proceeds of the sale.

- Interest Accrual: Interest is added to the loan balance over time, which means the amount owed increases as the years go by.

Want to learn more about Reverse Mortgage? Download your FREE Reverse Mortgage GUIDE.

Ready to Apply? You can now check your eligibility online or call Seniors First on 1300 745 745.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Please consult a licensed financial advisor before you make any decision.