For the past few years, many older Australians have benefited from the federal government’s freeze on deeming rates. This freeze meant that the income Centrelink assumed you earned from your savings and investments stayed artificially low, helping many retirees maximise their Age Pension.

But in September, the government announced Centrelink Age Pension changes that end this freeze. Deeming rates will gradually return to normal levels. While this may sound like a small technical adjustment, it has already had a real impact on pension payments and is contributing to cashflow pressure and financial stress for many seniors.

At Seniors First, we’ve been hearing from more older Australians who are suddenly finding their pension reduced—even though their actual income hasn’t changed at all.

Below, we explain what’s happened, provide simple examples of how this affects both full pensioners and part-pensioners, and share how safe equity-release solutions like a reverse mortgage may help ease the pressure.

What Are Pension Deeming Rates? (In Plain English)

Centrelink uses deeming rates to estimate how much income your financial assets are earning. These assets include:

- Savings accounts

- Term deposits

- Shares

- Managed funds

- Super (if you’re over Age Pension age)

Centrelink doesn’t look at your actual interest rate or investment return. Instead, they apply a set deeming rate, which is meant to reflect a reasonable earning rate.

For example, if you have $50,000 in the bank, Centrelink “deems” that it earns income at a certain percentage — even if you’re only getting 1.5% interest.

These deemed earnings count as income in the Age Pension income test. So if deemed income goes up, your pension can go down.

What changed with the Age Pension in September 2025?

The government ended the COVID-era freeze on deeming rates.

This means:

- Deeming rates will rise, and

- Deemed income for pensioners will be higher, even if your savings aren’t earning any more in reality.

For many seniors, this reduces pension entitlements by $10 to $60+ per fortnight, depending on assets.

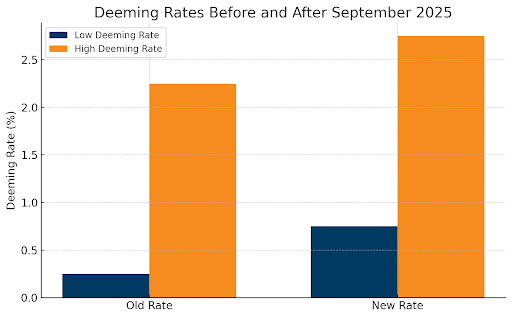

The low and high deeming rates are interest rates used to calculate the income from financial assets for Age Pension recipients; the low rate applies to the first portion of assets, while the high rate applies to amounts over a specific threshold. From September 20, 2025, the low deeming rate is 0.75% and the high deeming rate 2.75 %. The asset thresholds are $64,200 for singles and $106,200 for couples, above which the higher rate applies.

Why It Feels Unfair

Many seniors have told us:

“My pension went down, but I’m not earning any more!”

This frustration is understandable.

Deeming rates don’t reflect what banks are actually paying on savings right now, and they often don’t reflect the real-world return of conservative investments used by pensioners.

It’s a system designed for simplicity, but it can feel harsh when changes reduce your income even though your financial situation hasn’t improved.

Why the impact is meaningful

Because the upper deeming rate has increased from 2.25% to 2.75%, and the lower rate from 0.25% to 0.75% as of 20 September 2025. AMP+1

One source estimated: “for each $100,000 of financial assets, the fortnightly age pension entitlement will decrease by about $9.61” based on the increase in deemed income. SUPERCentral

That means if someone has $300,000 in add’l assets, they might see ~$28–30/week less pension — a meaningful figure for many retirees.

Example: How the Rise in Deeming Rates Can Reduce a Part-Pensioner’s Age Pension

Meet Alan (Single, Homeowner, Age 76)

Alan is on a part Age Pension and owns his home. He has:

- $260,000 in financial assets (term deposits + bank savings)

- No other assessable income

- Receives a part pension under the income test, because he is above the income-test “free area”

- The income-test free area for singles is $218 per fortnight

- Pension reduces by 50 cents for every $1 of income above that amount

Step 1: Deemed income before the deeming-rate increase (for comparison)

The previous deeming rates were:

- 25% (low rate)

- 25% (upper rate)

Calculation at old deeming rates:

- First $64,200 × 0.25% = $160.50 per year

- Remaining $195,800 × 2.25% = $4,405.50 per year

- Total = $4,566 per year (~$175.62 per fortnight)

This placed Alan below the income-test cut-off, so he qualified for a part Pension.

Step 2: Deemed income after the September increase

Current deeming rates (as of 20 Sept 2025):

- 75% (low rate)

- 75% (upper rate)

New calculation at higher deeming rates:

- First $64,200 × 0.75% = $481.50 per year

- Remaining $195,800 × 2.75% = $5,384.50 per year

- Total = $5,866 per year → approx $225.61 per fortnight

Step 3: How this affects Alan’s Age Pension

Under the income test, his pension reduces by:

- 50¢ for every $1 over the free area

- Income-test free area: $218 per fortnight

Before the deeming increase

- Deemed income: $175.62/fn

- Below $218 → No reduction

- Alan receives his usual part pension entitlement

After the deeming increase

- Deemed income: $225.61/fn

- Amount over free area: $225.61 − $218 = $7.61

- Pension reduction = 50% of $7.61 = $3.80 per fortnight

Alan’s Age Pension drops by $3.80 per fortnight.

That’s about $98.80 per year — even though his real savings haven’t increased at all.

Why This Matters

Alan is a textbook example of how the end of the deeming-rate freeze can reduce the pension for part-pensioners who:

- Sit just above the income-test free area

- Have moderate to higher levels of financial assets

- Rely on consistent pension payments to manage household bills

Even a small reduction can create cashflow strain, especially when combined with rising prices for insurance, utilities, food, rates, and medical costs.

How a Reverse Mortgage Can Help Supplement Age Pension – Ease Cashflow Pressure

For homeowners aged 60+, a reverse mortgage can be a practical way to boost cashflow without selling the family home.

A reverse mortgage allows you to unlock some of the equity in your home:

- as a lump sum,

- as a regular monthly top-up, or

- as a flexible cash reserve you draw on if needed.

The funds do not affect the Age Pension income test, because reverse mortgage advances are not treated as income by Centrelink (though amounts held in cash may become assets—your broker will guide you through this).

For someone already close to the income-test thresholds, this can be a practical, low-stress solution. A reverse mortgage could provide:

- $200–$400 per month extra to cover bills, or

- A small cash reserve to take the pressure off pension reductions

For pensioners who have been affected by the Centrelink Age Pension changes it might:

- Replace the pension income they lost

- Help maintain their quality of life

- Provide peace of mind during cost-of-living pressures

And most importantly — you continue living in your home for as long as you choose, provided you meet basic loan conditions such as maintaining the property and keeping it insured.

You Don’t Need to Struggle Alone

Many seniors feel anxious when their Age Pension drops unexpectedly — especially when they’ve always managed carefully and lived within their means.

If you’re feeling the pressure, a conversation with a specialist reverse mortgage broker can give you clear options tailored to your situation.

At Seniors First, we:

- Explain everything in plain English

- Compare lenders to find suitable products

- Help you understand how your pension might be affected

- Offer guidance with no obligation

Next Steps

If the end of the deeming rate freeze has reduced your pension and put pressure on your finances, we’re here to help.

Book a free, no-obligation consultation with a Seniors First reverse mortgage specialist.

We’ll take the time to understand your needs and help you explore safe, sensible solutions.

Disclaimer:

The information in this article is based on rules, thresholds and deeming rates current at the time of publication. It is provided for general information only and does not take into account your personal circumstances. It should not be considered financial advice, pension advice, or a substitute for guidance from a qualified professional. Age Pension entitlements can vary depending on your individual situation, and government policies may change. You should seek independent financial advice or contact Services Australia for information specific to your circumstances.

Good to know.