A new survey released by Deloitte provides one of the clearest snapshots yet of how Australians are actually using reverse mortgages in retirement.

For anyone considering accessing home equity, the findings are fascinating — and in some cases surprising. They reveal how much equity retirees are sitting on, how cautiously people are using reverse mortgages, and why the product is increasingly being used earlier in retirement.

For homeowners aged 60 and over who are exploring their financial options, these insights help explain how reverse mortgages are evolving from a niche product into a mainstream retirement planning tool.

Let’s unpack some of the most important findings — and what they really mean for retirees.

1. Australians Over 60 Are Sitting on $3 Trillion in Home Equity

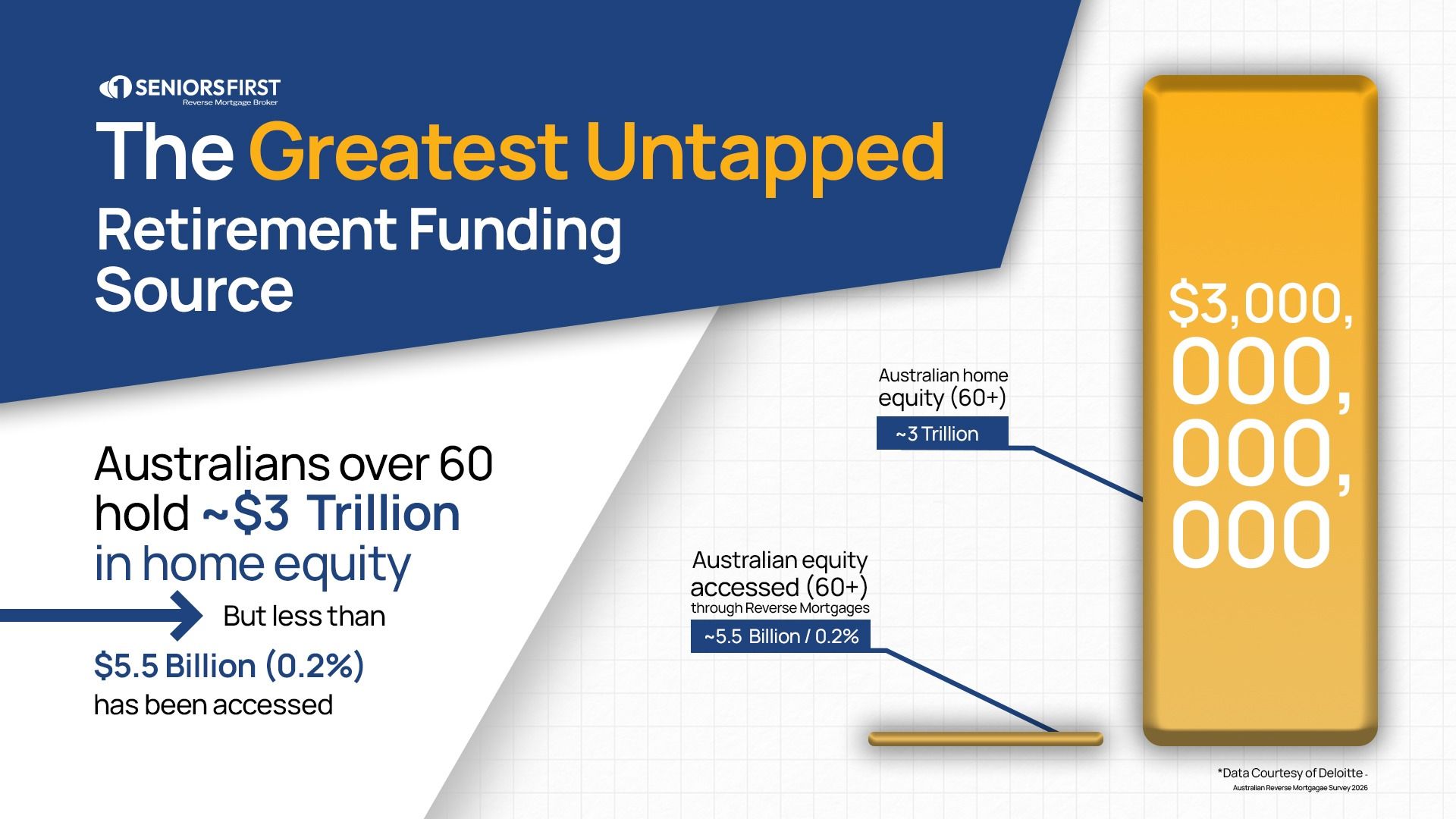

One of the most striking findings from the Deloitte survey is the scale of housing wealth among older Australians.

Australians aged 60 and over collectively hold around $3 trillion in home equity, with roughly $600 billion potentially accessible through equity release products like reverse mortgages. (deloitte.com)

Yet despite this enormous pool of wealth, only about 1% of that available equity has actually been accessed. (Deloitte)

What this tells us

This highlights one of the biggest structural issues in Australia’s retirement system:

Many retirees are asset rich but income poor.

They may own their home outright, but still face challenges funding everyday living expenses, renovations, healthcare costs, or helping family.

The survey suggests reverse mortgages remain significantly underused, largely because many homeowners either:

- don’t fully understand how they work

- worry about losing their home

- or simply haven’t explored the option yet

In reality, modern reverse mortgages in Australia are heavily regulated and designed to allow retirees to stay in their home while accessing some of its value.

2. Most Borrowers Access Far Less Equity Than They Could

Another interesting insight from the report is how conservatively borrowers use reverse mortgages.

The average loan amount is around $150,000, and most loans represent only about 15% of the property value. (Deloitte)

Even more interesting: many borrowers are accessing only about half of the equity they are eligible for.

What this tells us

This strongly challenges the old stereotype that reverse mortgages are used recklessly.

Instead, the data shows that retirees tend to use them very deliberately and selectively.

In practice, most borrowers use a reverse mortgage to solve specific financial challenges, such as:

- clearing remaining mortgage or credit card debt

- renovating their home to age safely in place

- replacing a vehicle

- supplementing retirement income

- funding travel or lifestyle goals

In other words, retirees are generally not drawing the maximum amount available — they are using home equity strategically.

3. Reverse Mortgages Are Increasingly Used Earlier in Retirement

Another key finding is the age profile of new borrowers.

The survey shows that 34% of new reverse mortgage customers are under 70, while only 15% are aged over 80. (Financial Standard)

What this tells us

Historically, reverse mortgages were often associated with very late retirement.

But that perception is changing.

Many Australians are now using home equity during the transition into retirement, particularly when:

- they reduce working hours

- superannuation drawdowns begin

- income becomes less predictable

Accessing a small portion of housing equity can provide a financial buffer, helping retirees manage cash flow without having to sell their home.

This shift reflects a broader trend in retirement planning:

housing wealth is increasingly being viewed as the third pillar of retirement, alongside superannuation and the Age Pension. (Deloitte)

4. A Surprising Statistic: Around 10% of Borrowers Make Voluntary Repayments

One of the most overlooked but important statistics in the survey is that around 10% of reverse mortgage borrowers make voluntary repayments each year. (Deloitte)

This is noteworthy because reverse mortgages do not require regular repayments.

Why this matters

The fact that many borrowers still choose to repay part of their loan indicates something important:

People are actively managing their reverse mortgage.

Voluntary repayments often happen when:

- retirees downsize later in life

- financial circumstances improve

- inheritances or asset sales occur

- borrowers simply want to reduce interest compounding

This behaviour suggests reverse mortgages are increasingly being used as a flexible financial tool, rather than a “set and forget” loan.

5. What Are People Actually Using Reverse Mortgages For?

The survey found that funds are most commonly used for: (Deloitte)

- Home improvements and renovations

- Paying off existing debts

- Lifestyle purchases such as cars or travel

- Supplementing retirement income

These uses reflect a simple reality of retirement finances.

For many Australians, their home is their largest financial asset, but it traditionally hasn’t been part of retirement planning.

Reverse mortgages change that by allowing homeowners to convert some of that housing wealth into usable funds — without selling their home.

6. The Big Opportunity: Awareness Remains Low

Despite the scale of the opportunity, the Deloitte report highlights a key issue:

Awareness of reverse mortgages remains surprisingly low.

Even among mortgage brokers and financial professionals, the product is still not widely discussed.

This means many retirees may be missing a potentially useful option when considering:

- downsizing

- selling investments

- drawing down super faster than planned

For some homeowners, accessing a small portion of home equity may provide a simpler alternative.

Final Thoughts: A More Mature Reverse Mortgage Market

The Deloitte findings paint a very different picture from the outdated myths around reverse mortgages.

The data suggests borrowers today are:

- using the product cautiously

- borrowing relatively small amounts

- accessing equity earlier in retirement

- and in many cases making voluntary repayments

In short, reverse mortgages are increasingly being used as a strategic retirement planning tool, rather than a last resort.

For homeowners approaching retirement, the key question is no longer simply:

“Should I use my home equity?”

But rather:

“How can my home equity work alongside my superannuation and pension to support the retirement I want?”

If you’re exploring whether a reverse mortgage might suit your situation, speaking with a specialist broker can help you understand how it works, how much you could access, and whether it aligns with your long-term plans.

Book a confidential discussion with the team at Seniors First to explore your options.

Hi,

Can I use the equity in my home to get an advance I can use towards the purchase of a new home?

Elisa

Hi Elisa, yes it is possible but it will depend on the situation. It may be that a bridging loan is more suitable.